FATCA Reporting for U.S. Taxpayers

Brief Overview of FATCA

The Foreign Account Tax Compliance Act (FATCA) represents a crucial component of U.S. tax law aimed at combating tax evasion on a global scale. Enacted in 2010, FATCA requires U.S. taxpayers to report their financial accounts held outside the United States, promoting transparency and ensuring compliance with tax obligations. The significance of FATCA reporting extends beyond domestic borders, fostering cooperation among international financial institutions to facilitate the exchange of information with the Internal Revenue Service (IRS).

Importance of FATCA Reporting for U.S. Taxpayers

FATCA reporting holds paramount importance for U.S. taxpayers due to its impact on financial transparency and tax compliance. By mandating the disclosure of foreign financial accounts, the legislation aims to deter tax evasion, identify unreported income, and ensure that taxpayers fulfill their obligations to the U.S. government. Failure to comply with FATCA reporting requirements may result in penalties, emphasizing the need for individuals to understand and adhere to the provisions of this regulatory framework.

Under FATCA, U.S. taxpayers with financial assets situated outside the United States are obligated to disclose these assets to the IRS using Form 8938, known as the Statement of Specified Foreign Financial Assets. Failure to comply with this reporting requirement may result in substantial penalties, as outlined below. Notably, this FATCA mandate is distinct from the longstanding obligation to report foreign financial accounts through FinCEN Form 114, previously known as Report of Foreign Bank and Financial Accounts (FBAR).

Additionally, FATCA imposes an obligation on specific foreign financial institutions to directly report to the IRS details regarding financial accounts held by U.S. taxpayers or by foreign entities with substantial ownership ties to U.S. taxpayers. These reporting entities encompass not only banks but also extend to various financial institutions, including investment entities, brokers, and specific insurance companies. Certain non-financial foreign entities are also subject to reporting requirements for their U.S. owners.

As a result, when establishing a new account with a foreign financial institution, you may be required to provide information about your citizenship. FATCA introduces modified and reduced reporting standards for U.S. account holders of certain financial institutions that operate exclusively within their country of organization and primarily serve account holders residing within that jurisdiction. To qualify for this preferential treatment, the local foreign financial institution must refrain from discriminatory practices, such as refusing to open or maintain accounts for U.S. citizens residing in the country of its organization.

What is FATCA?

FATCA, enacted as part of the Hiring Incentives to Restore Employment (HIRE) Act, is designed to address tax evasion by requiring foreign financial institutions (FFIs) to report information about financial accounts held by U.S. taxpayers. Additionally, U.S. taxpayers themselves are obligated to disclose their foreign financial holdings and accounts to the IRS.

Who is Required to Report under FATCA?

FATCA mandates that specific U.S. taxpayers holding foreign financial assets exceeding the reporting threshold (a minimum of $50,000) must disclose details about these assets on Form 8938. This form must be appended to the taxpayer’s annual income tax return. It’s worth noting that the reporting threshold varies for certain individuals, including married taxpayers filing a joint annual income tax return and certain taxpayers residing in a foreign country (refer to details below).

Foreign Financial Institutions (FFIs): FFIs, including banks, investment entities, and certain insurance companies located outside the United States, are required to report information about financial accounts held by U.S. taxpayers.

U.S. Taxpayers: U.S. citizens, resident aliens, and certain non-resident aliens with specified financial interests in or signature authority over foreign financial accounts must report these accounts to the IRS.

As of January 2013, only individuals are required to report their foreign financial assets. At a later time, a limited set of U.S. domestic entities also may have to report their foreign financial assets, but not for tax years starting before 2013. There are some exceptions to the requirement that you file Form 8938. For example, if you do not have to file a U.S. income tax return for the year, then you do not have to file Form 8938, regardless of the value of your specified foreign financial assets. Also, if you report interests in foreign entities and certain foreign gifts on other forms, you may just list the submitted forms on Form 8938, without repeating the details.

Types of Foreign Financial Accounts Covered

FATCA reporting encompasses various types of foreign financial accounts, including but not limited to:

- Bank Accounts: Checking and savings accounts held in foreign financial institutions.

- Investment Accounts: Securities and brokerage accounts located outside the United States.

- Mutual Funds: Ownership interests in foreign mutual funds or similar pooled funds.

- Insurance or Annuity Policies: Certain insurance or annuity policies with a cash value.

Reporting Thresholds and Requirements

Thresholds for Reporting

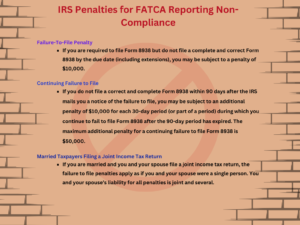

The reporting thresholds are contingent upon whether you file a joint income tax return or reside abroad. If you are single or file separately from your spouse, submission of Form 8938 is required if, by the end of the year, you have more than $200,000 in specified foreign financial assets and live abroad, or more than $50,000 if you reside in the United States. When filing jointly with your spouse, these thresholds double. Living abroad is defined as being a U.S. citizen with a tax home in a foreign country and a presence in a foreign country or countries for a minimum of 330 days within a consecutive 12-month period.

For taxpayers residing abroad, Form 8938 must be filed if an income tax return is required, and:

- You file a joint income tax return and the total value of specified foreign financial assets exceeds $400,000 on the last day of the tax year or surpasses $600,000 at any time during the year. These thresholds apply even if only one spouse resides abroad. Married individuals filing jointly will submit a single Form 8938 reporting all specified foreign financial assets in which either spouse has an interest.

- You are not married filing a joint income tax return, and the total value of specified foreign financial assets is more than $200,000 on the last day of the tax year or exceeds $300,000 at any time during the year.

For taxpayers residing in the United States, Form 8938 must be filed if an income tax return is required, and:

- You are unmarried, and the total value of specified foreign financial assets is more than $50,000 on the last day of the tax year or surpasses $75,000 at any time during the tax year.

- You file a joint income tax return, and the total value of specified foreign financial assets is more than $100,000 on the last day of the tax year or exceeds $150,000 at any time during the tax year.

- You file separate income tax returns, and the total value of specified foreign financial assets is more than $50,000 on the last day of the tax year or surpasses $75,000 at any time during the tax year. When calculating the value of specified foreign financial assets for this threshold, include one-half the value of any jointly owned asset with your spouse. However, report the entire value on Form 8938 if filing Form 8938 is mandatory.

Thresholds: U.S. taxpayers must report foreign financial accounts if the aggregate value exceeds specific thresholds, which vary depending on filing status and location.

Form FinCEN 114 (FBAR) and Form 8938: Reporting is typically done through the Report of Foreign Bank and Financial Accounts (FBAR) on FinCEN Form 114 and Form 8938, Statement of Specified Foreign Financial Assets, filed with the individual’s federal income tax return.

Exceptions to Reporting Requirements

You are exempt from reporting specified foreign financial assets again on Form 8938 if you have already reported them on other forms. These exceptions encompass interests in:

- Trusts and foreign gifts, previously reported on Form 3520 or Form 3520-A (filed by the trust).

- Foreign corporations, disclosed on Form 5471.

- Passive foreign investment companies, reported on Form 8621.

- Foreign partnerships, reported on Form 8865.

- Registered Canadian retirement savings plans, reported on Form 8891.

While the value of foreign financial assets reported on these forms is factored into determining the total value of assets for the reporting threshold, you are not required to list these assets again on Form 8938. In such cases, indicate on Form 8938 which specific form(s) report the specified foreign financial assets and the quantity.

Additional exemptions from reporting are granted for certain trusts, certain assets held by bona fide residents of U.S. territories, and assets or accounts for which mark-to-market elections have been made under Internal Revenue Code Section 475. For instance, a U.S. beneficiary of a domestic bankruptcy trust or a domestic widely held fixed investment trust is not obligated to report any specified foreign financial asset held by the trust on Form 8938.

Asset Valuation

To ascertain whether the total value of your specified foreign financial assets surpasses the applicable threshold, it is essential to determine their value. Generally, for reporting purposes, a reasonable estimate of the highest fair market value of the asset during the tax year is provided, with special rules in place to alleviate valuation complexities.

For financial accounts, the maximum value can be derived from periodic financial account statements (issued at least annually). In the case of a specified foreign financial asset not held in a financial account, the year-end value may be relied upon if it reasonably approximates the asset’s maximum value during the tax year. Special rules also govern reporting the maximum value of interests in foreign trusts, foreign retirement plans, or foreign estates.

Fair market value can be determined based on information publicly available from credible financial sources or other verifiable sources. Even in the absence of information from reliable financial sources, a reasonable estimate of fair market value suffices for reporting purposes.

When dealing with assets denominated in a currency other than U.S. dollars, use the foreign currency exchange rates provided by the U.S. Department of the Treasury’s Bureau of the Fiscal Service to convert the denomination into U.S. dollars. If a specific currency’s exchange rate is unavailable there, employ another publicly available foreign currency exchange rate to convert the specified foreign financial asset’s value into U.S. dollars. The exchange rate is determined based on the rate applicable on the last day of your tax year.

Penalties for Failure to Report

Failure to Comply with Form 8938 Reporting Obligations

In the event that you are required to file Form 8938 and neglect to do so, penalties may be imposed, including a $10,000 failure-to-file penalty. Furthermore, an additional penalty of up to $50,000 may be levied for persistent failure to file, especially following notification from the IRS. Additionally, a 40 percent penalty on any tax understatement attributable to undisclosed assets may be incurred. ( see below for more detail)

The statute of limitations is prolonged to six years after filing your return if an omission from gross income, exceeding $5,000 and linked to a specified foreign financial asset, occurs regardless of the reporting threshold or any reporting exceptions. Should there be a failure to file or appropriately report an asset on Form 8938, the statute of limitations for the respective tax year extends to three years after providing the required information. In cases where the failure is attributed to reasonable cause, the statute of limitations only extends for the specific item or items associated with the failure and not for the entire tax return.

It’s noteworthy that if you can demonstrate that any failure to disclose is rooted in reasonable cause and not due to willful neglect, no penalty will be imposed for the failure to file Form 8938. The determination of reasonable cause is made on a case-by-case basis, taking into account all relevant factors.

Failure to comply with the reporting requirements under the Foreign Account Tax Compliance Act (FATCA) can lead to significant penalties for both foreign financial institutions (FFIs) and U.S. taxpayers:

FFIs Penalties: Foreign financial institutions that do not fulfill their reporting obligations may face a 30% withholding tax on certain U.S.-source payments. This penalty is a powerful incentive for FFIs to adhere to FATCA reporting requirements.

U.S. Taxpayers Penalties: U.S. taxpayers failing to report their foreign financial accounts may be subject to various penalties. These penalties can include substantial fines based on the aggregate value of the undisclosed accounts and can be as high as 50% of the account balance.

Legal Implications for Non-Compliance

Criminal Prosecution: Willful non-compliance with FATCA reporting requirements may result in criminal prosecution. Individuals convicted of tax evasion or other related offenses may face imprisonment, fines, or both.

Civil Lawsuits: Non-compliance may expose individuals and entities to civil lawsuits, including actions brought by the U.S. government. Such lawsuits may seek the recovery of unpaid taxes, penalties, and interest.

Revocation of Financial Institution Status: Foreign financial institutions that repeatedly fail to meet FATCA reporting obligations may face the revocation of their status as participating FFIs. This can have severe consequences for the institution’s ability to conduct certain financial transactions and business activities.

Loss of Financial Services: Non-compliant U.S. taxpayers may find themselves subject to increased scrutiny from financial institutions, making it challenging to access certain financial services. This can include restrictions on opening new accounts or obtaining loans.

Reputational Damage: Non-compliance with FATCA can lead to reputational damage for both individuals and institutions. Negative publicity surrounding legal actions, fines, or penalties may harm professional and personal reputations.

It is crucial for both foreign financial institutions and U.S. taxpayers to understand and adhere to FATCA reporting requirements to avoid these serious consequences. Seeking professional advice and ensuring compliance with the law can mitigate the risks associated with non-compliance and contribute to a transparent and accountable financial environment.

Key Steps in FATCA Reporting

Gathering Necessary Information

- Collecting Account Information: identify and compile information about all foreign financial accounts, including bank accounts, investment accounts, and other specified financial assets.

- Documenting Account Details: Record account numbers, names of financial institutions, and the maximum values of each account during the reporting period.

- Verification of Reporting Thresholds: Verify whether the aggregate value of foreign financial accounts meets the reporting thresholds set by the Internal Revenue Service (IRS) based on filing status and location.

Completing Form 8938

Determine Filing Requirement: Assess whether you meet the filing requirements for Form 8938, “Statement of Specified Foreign Financial Assets.”

Accessing the Form: Download Form 8938 from the IRS website or use tax preparation software that supports FATCA reporting.

Provide Required Information: Complete the form by entering accurate details about each specified foreign financial asset, including the type of asset, its maximum value, and other relevant information.

Attach Form to Tax Return: Attach the completed Form 8938 to your annual federal income tax return. Ensure that it is filed by the appropriate deadline, typically the same date as your income tax return.

Reporting through the Foreign Bank Account Report (FBAR)

Determine FBAR Filing Requirement: Assess whether you meet the filing requirements for the Report of Foreign Bank and Financial Accounts (FBAR).

Accessing the FBAR Form: File the FBAR electronically through the Financial Crimes Enforcement Network (FinCEN) website. Ensure that you use the most up-to-date version of the FBAR form.

Provide Account Information: Enter detailed information about each foreign financial account, including the account number, name and address of the financial institution, and maximum value of the account during the reporting period.

Verify Filing Deadline: Be aware of the FBAR filing deadline, which is typically April 15 but can be extended to October 15. Ensure that the FBAR is submitted timely to avoid penalties.

Keep Records: Maintain records of the FBAR submission, including confirmation receipts and any supporting documentation. This documentation is essential in case of future inquiries.

The importance of FATCA reporting cannot be overstated in the realm of international tax compliance. FATCA serves as a crucial tool in the fight against tax evasion, fostering transparency in global financial transactions. The reporting requirements for both foreign financial institutions (FFIs) and U.S. taxpayers play a pivotal role in creating a robust framework that deters illicit financial activities and ensures the proper fulfillment of tax obligations. FATCA reporting is integral for the following reasons:

Enhanced Financial Transparency: Reporting under FATCA enhances transparency by requiring the disclosure of foreign financial accounts, discouraging individuals and institutions from concealing assets and income.

Global Cooperation: FATCA promotes international cooperation by establishing mechanisms for the exchange of financial information between the U.S. and other countries. This collaborative effort strengthens the effectiveness of tax enforcement on a global scale.

Deterrence of Tax Evasion: The stringent penalties associated with non-compliance serve as a powerful deterrent against tax evasion, encouraging compliance with reporting obligations.

Fair Taxation: By ensuring that U.S. taxpayers report their foreign financial holdings, FATCA contributes to a fair and equitable tax system, where all individuals are held accountable for their financial activities.

Encouragement for Proactive Reporting

As we navigate the complexities of the global financial landscape, it is essential for all relevant parties, including foreign financial institutions and U.S. taxpayers, to approach FATCA reporting proactively. Embracing this proactive stance involves:

Understanding Reporting Obligations: Stay informed about the specific reporting requirements applicable to your situation. Awareness of these obligations is the first step toward compliance.

Timely and Accurate Reporting: Adhere to deadlines and ensure that reporting is accurate and comprehensive. Timely and accurate reporting not only fulfills legal requirements but also contributes to the effectiveness of the entire reporting framework.

Seeking Professional Guidance: Given the complexities of tax laws and reporting requirements, seek professional advice to navigate the intricacies of FATCA reporting. Tax professionals can provide valuable insights and ensure compliance with evolving regulations.

Embracing a Culture of Compliance: Foster a culture of compliance within financial institutions and among individuals. Proactive reporting is not only a legal obligation but also a commitment to ethical financial practices.

In adopting a proactive approach to FATCA reporting, we contribute to the integrity of the global financial system, support fair taxation, and collectively work towards a more transparent and accountable financial environment. By fulfilling our reporting obligations, we play a vital role in upholding the principles of fiscal responsibility and ethical financial conduct.

-

Pane How Often Should Taxpayers Update Their Information?

Taxpayers should update their information whenever there are changes to their foreign financial accounts. Changes may include opening or closing accounts, significant changes in account values, or other modifications that affect the accuracy of the reported information. Regularly reviewing and updating information ensures compliance with FATCA reporting requirements.

-

What to Do in Case of Errors in Reporting?

In case of errors in FATCA reporting, taxpayers should take corrective action promptly:

Amendments (Form 8938): If errors are discovered after filing Form 8938, taxpayers can file an amended return to correct the inaccuracies. This should be done as soon as the errors are identified.

Amending FBAR: To correct errors on the FBAR, taxpayers should file an amended FBAR as soon as possible. Use the FBAR e-filing system to submit the corrected information electronically.

-

What is the Deadline for FATCA Reporting?

The deadline for FATCA reporting depends on the specific reporting requirement:

Form 8938 (Filed with Tax Return): Form 8938 is typically filed with an individual’s annual federal income tax return. The deadline for filing the tax return, including Form 8938, is generally April 15. However, it can be extended to October 15 if an extension is requested.

FBAR (Foreign Bank Account Report): The FBAR is due by April 15, with an automatic extension available until October 15. Unlike Form 8938, the FBAR is filed separately from the tax return and is submitted electronically through the Financial Crimes Enforcement Network (FinCEN) website.

It’s crucial to be aware of and adhere to these deadlines to avoid penalties associated with late filing.

{kind=link}